Making sense of trade policy directions in budget

Annual budgets are widely reported and its components hotly debated, as it usually provides insights on the direction of overall public policy that impinges on a broad spectrum of our lives and livelihoods. It is not merely a statement of fiscal policy but a declaration of overall economic strategy for the coming year and beyond. Though five-year plans provide the broad framework of medium-term economic strategy in practice it is clearly the budget numbers that are of more consequence than the targets and policy instruments laid out in the five-year plans.

The FY2019 budget is no exception. We all expected it to be an election-year budget. And so it is. Undertaking reforms entails political risks and often triggers controversy. The budget, therefore, stays clear of any serious risk-prone reform action this time. That the policy stance for the coming year leaves the much reported financial sector woes untouched is an act of omission that by all accounts is apt to impose heavy costs on the economy in the medium-term. We should all hope that after elections restoring sanity to the financial sector would be the first order of business for the new government.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. The least discussed aspect of the budget appears to be its trade policy component. Yet every budget comprises a trade policy stance that has serious ramifications for trade and industry incentives and the returns on investment. The budget actually lays out the direction for trade policy, i.e. the domestic policy content of how exports will be incentivised and imports will be managed through the imposition of tariffs and para-tariffs. Though the tri-annual Import Policy Order and Export Policy framed by the commerce ministry make up the regulatory regime for import-export transactions, the fact that quantitative restrictions on imports no longer exist for protection purposes, these orders no longer constitute trade policy per se. Let's not forget that trade policy does matter, for rapid export-oriented industrialisation and accelerated economic growth.

In the realm of trade policy, policymakers face two national imperatives: (a) to expand and diversify our exports, and (b) to rationalise our industrial protection regime to remove anti-export bias of incentive policies.

After more than two decades of double digit export growth, this particular leading indicator of our economy is faltering. Exports in FY2018 are expected to record a meagre 7 percent growth at about $37 billion, well below the volume and growth target set under the 7th Five-Year Plan. This happens at a time when Vietnam's well diversified exports reached a record $214 billion in 2017, up a record 21 percent compared to 2016, according to Vietnam's General Statistics Office.

Vietnam has also been raising its share in the US market to 11-12 percent when Bangladesh's share has remained static at 5 percent. That should set off alarm bells. A change of course in trade policy coming out of the budget statement was reasonable to expect. But that did not happen.

This came at a time when the global context for export expansion from developing countries is facing strong headwinds stemming from the protectionist sentiments unleashed by the 'America First' tirade on the one hand and the populist upsurge in many European countries castigating globalisation and free trade on the other.

Though the world economy is not yet out of the "slow growth" syndrome, the latest version of the International Monetary Fund's Global Economic Outlook is projecting modest uptick in global growth of output as well as trade. What this means for Bangladesh exports is that while there are challenges ahead, global demand for Bangladesh's exports should remain steady in the near to medium-term. That is because Bangladesh is technically a small economy in global trade and should be able to sell all its exports in the world market provided they are cost competitive. So, the trade policy challenge for Bangladesh policymakers is to maintain export momentum by ensuring cost competitiveness.

The FY2019 budget's trade policy stance can be gleaned from the following propositions contained in the budget speech of the finance minister: (a) to keep the prices of essential goods unchanged; (b) to provide necessary protection to domestic industries; (c) to expedite expansion of exports; and (d) to rationalise the tariff structure by reducing prevailing discrepancies. Reviewing these propositions in light of the budget numbers yields the following assessment of trade policy stance.

First, with the passing of time, there is a clear need to rethink our definition of 'essential goods' and make a general proposition about 'consumer goods' that are bought by the average consumer in Bangladesh.

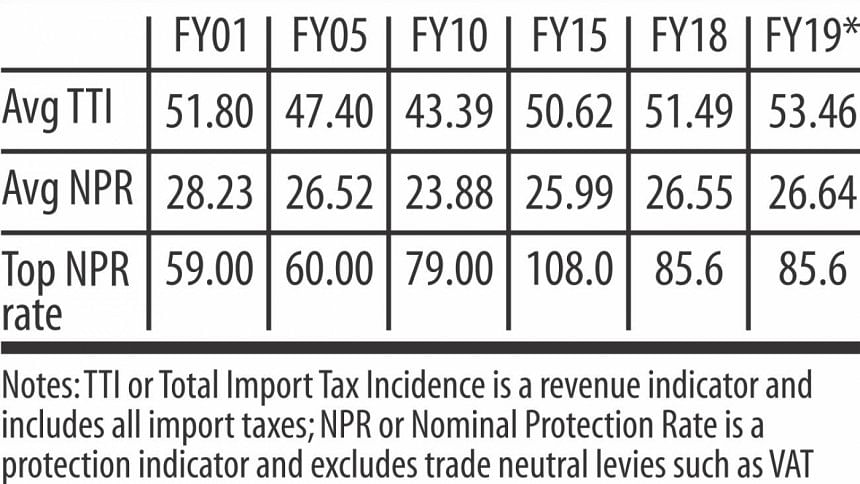

Prices of these consumer goods are directly impacted by the high rates of import tariffs that prevail so much so that PRI research shows that Bangladeshi consumers pay prices roughly 50-100 percent above international prices for most manufactured consumer goods. Leaving these prices unchanged means leaving the price level significantly higher than the price level in comparator countries making Bangladesh appear to be a rather expensive place for most consumer goods. This election-year budget should have taken a step forward to dismantle the high tariffs and bring down the price level of most consumer goods.

Second, while protection to domestic industries has become a strongly entrenched policy, it ignores the fact that domestic industries produce for exports as well as for sale in the domestic market (mostly import substitute products). Protective tariffs on import substitute production are indirect subsidies as they help raise the price of import substitutes in the domestic market. These subsidies are actually paid not out of the budget but by unsuspecting consumers in the marketplace. It is the high rate of protective tariffs and the never-ending stance of industrial protection that has become a long-lasting burden (protection tax) on Bangladeshi consumers. Simple logic as well as empirical evidence around the world tells us that protection ad infinitum is never a good policy. Lulled by high protection these import substitute industries are unlikely to become globally competitive in order to become significant exporters. Our garment industry was never an import substitute industry. A start towards rationalisation of the protection regime could have been made in this budget.

Third, expansion of exports and its diversification is an oft-repeated message that can be heard round the year – also emphasised in all budget speeches. But the trade policy stance appears to favour import substitute production (for sales in the domestic market) more than exports. How? Protective tariffs are so high that they make domestic sale of import substitute products much more profitable than exports. Where export subsidies for a few selected export products range from 5 percent to 20 percent, protective tariffs on import substitute consumer goods range from 40 percent to more than 100 percent. While 100 percent export-oriented garment industries are not exposed to this perverse incentive, domestic industries that cater to exports and domestic sales face the dilemma. Export production and investment in non-garment industries are consequently inhibited. Export expansion and diversification suffer. The budget should have at least recognised this imbalance of incentives between exports and domestic sales.

Fourth, the goal of rationalisation of the tariff structure appears sensible but the task is daunting given the extent of the problem and the history of tariff setting. Tariff rates and complexity of the tariff structure need to be rationalised. There is no reason why Bangladesh should have the highest average rates of tariffs among comparators.

The tariff situation remains broadly unchanged though the budget speech acknowledges the occasional use of regulatory duty (RD) and supplementary duty (SD) for revenue purposes. However, PRI research has shown that 95 percent of SDs are actually protective duties, with the exception of those imposed on automobiles, alcoholic beverages, tobacco, and firearms.

SDs are less effective in mobilising revenue. So, eliminating these SDs or making them trade-neutral (as was stipulated in the aborted 2012 VAT Law) would be the first order of business in a trade policy reform agenda if it ever comes to pass.

The overall vision in the FY2019 budget appears broadly consistent with the goals laid down in the 7th Five-Year Plan, in respect of GDP growth, inflation, fiscal deficit, and investment. But that is where the consistency ends. The budget seems to lack a trade policy orientation of the growth process and appears to fall short of the 7th Plan's trade policy orientation for rationalising protection in order to boost exports.

While industrial protection seems to have been given a free reign in the budget speech, it would have made good sense to provide the underlying rationale for prolonged protection of industry without any reference to a timeline. In the absence of such signals to the business community we are left wondering if the trade policy component in the budget reflects progress in this critical aspect of public policy.

The writer is the chairman of the Policy Research Institute of Bangladesh.

Comments