Higher NPL burden for banking sector

The banking sector is burdened by a high non-performing loan (NPL) and will need to continue measures to beef up supervision and accelerate loan recovery, according to the Bangladesh Bank.

The BB has taken an active role in amending the existing Bank Company Act, 1991 to tackle the challenges associated with the high NPL, the central bank said in its "Bangladesh Bank Quarterly" for the January-March period.

For all latest news, follow The Daily Star's Google News channel.

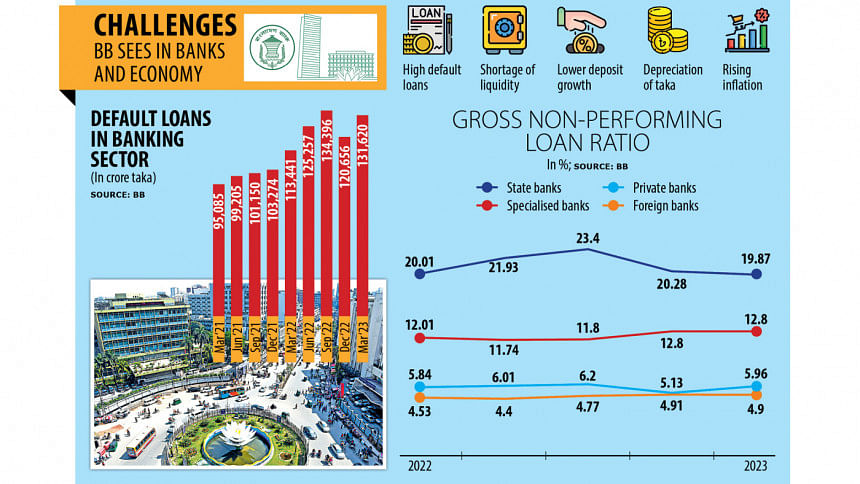

For all latest news, follow The Daily Star's Google News channel. NPLs stood at Tk 131,621 crore as of March 31, up 9 per cent from three months ago and 16 per cent from a year earlier, data from the BB showed.

The NPL figure is the second-highest in the banking sector's history and comes within a whisker of touching the all-time high of Tk 134,396 crore reported in the July-September quarter of 2022.

In March, the NPL ratio accounted for 8.8 per cent of the banking system's outstanding loans of Tk 14,96,346 crore. It was 8.16 per cent in December and 8.53 per cent in March last year.

Zahid Hussain, a former lead economist of the World Bank's Dhaka office, says that it is tough to find out a remarkable measure that has been taken by the central bank to bring down NPLs.

"Rather, the central bank has taken several measures in recent years that have pushed up default loans. Besides, the latest amendment to the Bank Company Act, 1991 may weaken the financial health of the banking sector."

He said the central bank has been offering defaulters and borrowers the scope to repay loans in a relaxed manner since 2015-16.

Parliament passed the new Bank Company Act on June 21, defining habitual defaulters for the first time.

As per the law, an individual will be considered a willful defaulter if he or she does not repay a loan obtained in their name or their company's name despite having the means to pay back.

In addition, a person will be treated as a habitual defaulter if they obtain loans under the name of non-existent firms or transfer assets kept as a collateral in a bank without its prior approval with a view to getting funds from others.

But Hussain says that the government has not kept any strong provision in the law to bring habitual defaulters to book.

The new law will allow a subsidiary of a group of companies to take loans even if other concerns default on loan payments.

Such facility was absent in the past, the economist said.

The law allows directors to remain on the board for up to 12 years from nine years previously, a provision that Hussain thinks will deal a blow to the corporate governance of the banking sector.

He said the law also did not address how to stop directors from one bank to secure credit facilities from others through mutual understanding.

Some directors usually take loans from the banks where they do not hold the post of directors. Such board members have already taken a large amount of loans thanks to mutual understanding among each other, creating concerns over corporate governance.

Ahsan H Mansur, executive director of the Policy Research Institute of Bangladesh, says that there has been no visible measure on the part of the central bank to arrest default loans.

"Political reason is the main factor behind the rise in NPLs."

In its publication, the central bank said the lower growth in bank deposits coupled with the gradual tightening of liquidity conditions and substantial depreciation of the taka may put further challenges for the banking sector.

It also said the economy faces two critical challenges that demand immediate attention: rising inflation and the exchange rate pressure.

The Consumer Price Index rose 9.02 per cent in 2022-23 against the government's revised target of 7.5 per cent. This was the highest average inflation rate in 12 years.

The taka has lost its value by about 25 per cent against the US dollar in the past one year owing to the sharp fall in the foreign currency reserve.

The BB said it has introduced several key measures to stabilise prices and exchange rates.

"By adopting a market-oriented framework, the BB seeks to maintain a delicate balance between promoting economic growth and maintaining price stability."

Comments