Angel investing 101: Doing it right in Bangladesh

As interest in the Bangladeshi startup ecosystem has grown, so has the responsibility of angel investors and other early stage stakeholders to properly assist founders and startups in preparing for their next stages of growth and funding. At Anchorless Bangladesh, we've spent the last 18 months better understanding how to accelerate the ecosystem relative to regional peers. This included a wide sweep with our friends at LightCastle Partners into the amount, type, and sources of funding for startups. Of the roughly US$300 million invested in startups so far, under $25 million came from angels, of which less than a third were from local angels.

In our assessment, the lack of consistent and appropriately structured angel funding is one of the single biggest weaknesses that has limited the development of the ecosystem. In comparison, our regional peers in India, Indonesia, and Vietnam have benefitted from angels playing a critical role in the early development and future funding of startups. Not only does Bangladesh need more angel investors, but we need those who do become angels to invest more effectively and thoughtfully so founders can proceed to raise future rounds of funding abroad to scale their businesses. Why does this matter? Because startups and venture capitals can have a generational impact on the Bangladeshi economy, paving the pathway for our own Google, Facebook, and Microsoft.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

The role of angels in the funding process

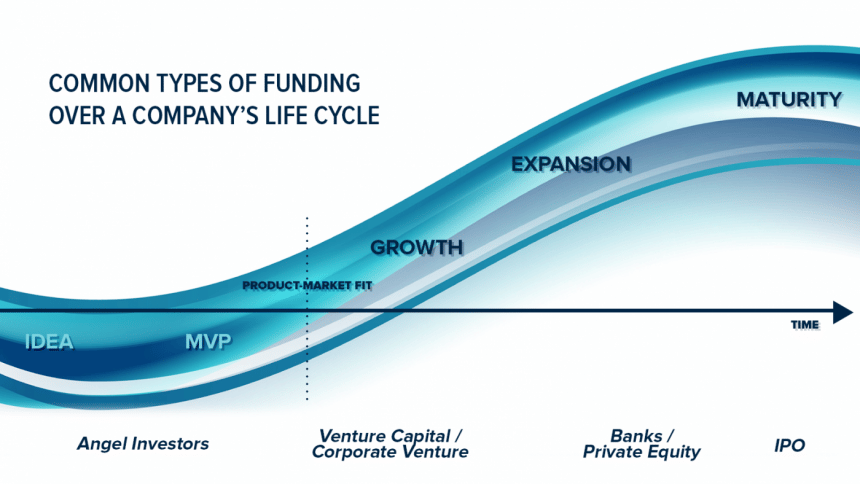

Angel investors give startups capital at very early stages — often even before the company has revenue, traction, or even a minimum viable product (MVP). While there are cases where angels invest in just an idea, especially for second or third-time founders with a track record, this is rare. A traditional startup's life cycle is shown below:

Angels are critical in supporting startups before they receive proper seed funding, when ideally an institutional investor would come in with sizable capital to aggressively go for product-market fit and scaling. Angels invest in startups to lock-in a disproportionately high return in return for the risk they take. For instance, well-known angel investor Jason Calacanis received a return of over $100 million for the $25,000 he initially put in. We encourage angel investors to build rapport with founders and the ecosystem; once an angel is known to properly support founders, they will likely get access to more future deals from the best founders. This explains why some angel investors get repeated deal flow into the best startups.

FINDING THE RIGHT INVESTMENT

The process of finding the right founders and funding the startups is not easy—however, if done right, the chances of a better return are significantly greater. Here are some suggestions for angel investors on how to find the next investment.

Quality of the founder and their focus

Finding the right investment starts with talking to founders. When we at Anchorless meet with companies, a sizable portion of our interest is related to the founders themselves. Similarly, an angel also invests in founders. Why? Because at the early stage of a startup, there's a lot of uncertainty regarding the market and the solution. This is exactly why an investor must trust founders to navigate such complexities. Before an investor puts in a dollar, they must make sure they're betting on those they trust and whose values and goals they align with — especially since an investment can last anywhere from 3-5 years, maybe even longer. Good founders will take capital and use it effectively to create value. If they are jumping from idea to idea without market research and validation, that may be a red flag.

Unit economics & tech-enabled scaling

While a startup will almost always be initially unprofitable, that doesn't mean it shouldn't have a strategy to improve its unit economics. It's a good sign when each successive sale the startup makes loses less money than the previous sale. One way to improve unit economics and scale efficiently is by having founders who have built or are capable of building a tech-enabled process that allows for the company to grow faster as it gets more customers. For instance, if a company needs to hire a new person for every new sale, then it's likely that the founders do not have a clear strategy on how to scale.

Market size and potential

During due diligence, investors should confirm that there is a reasonable market size for the product or service that the founders are envisioning. In addition, ask them, "What would you do if you had 100% market share?" This will show you how they think beyond their current business.

Valuing the investment

While there are no hard and fast rules for valuing an angel investment, taking a mid-to-long-term view here is necessary to ensure a positive outcome. The goal of an angel should be to make sure the company is properly set up for the next round of funding.

Exit strategy

Angel investors need to understand how their capital fits into the larger scheme of the fundraising process. Angels need to structure their involvement in a way from the beginning that allows a startup to successfully raise capital from institutional funds, likely from abroad, in a future round. We stress the importance of doing things the right way early so that an angel investor has a clearer path in actualising a return—or, in other words, get money back for the investment. In order to do this, angel investors must be able to sell their shares into the market either through an acquisition, secondary sale, or IPO. It's important to gauge the possibility of these options for each company.

CURRENT ISSUES WITH ANGEL INVESTING

Prospective investors not only need to assess startups with the right criteria but also need to evaluate their own motivations so that they can provide the kind of capital and support. Before getting into angel investing, prospective investors must ask themselves why they want to invest: Is it financial gain? If so, what is your time horizon? Is it personal satisfaction? Maybe a story to tell at a dinner party? Is it to show support to the community? How important is the return?

"Am I interested in investing in a startup or an SME?" This reflection is critical; the inability to understand the difference between the two has caused significant issues between investors and founders and, at times, negatively impacted the ecosystem's progress. Capital should only be allocated to a startup when the goals and vision of the investor and the founders are aligned.

The following is a compilation of issues based on feedback from local founders currently affecting the Bangladeshi angel investment scene:

• Angels taking more than around 20% of companies: As a startup is expected to raise multiple rounds of capital, it's important that the founders retain a sizable portion of the equity in order to remain incentivised. We have repeatedly seen that founders who own a larger part of their company will work on its success more than founders who own a small percentage of a startup. The chart below shows a breakdown of the mean and median stakes taken at each round; globally, angels usually do not take over 15% in the initial round. Due to the risky nature of the Bangladeshi ecosystem, taking a slightly higher percentage within reason is understandable. Ultimately, an angel investor's goal is to get the highest absolute dollar return regardless of percentage; 5% of $100 million is preferable to 20% of $10 million

• Angels taking board control: In short, when an institutional investor (such as a venture capital fund) invests in a company, it wants to make sure the founders are in control of their company instead of an early angel who came in with a relatively small amount of early capital — especially when they are looking to put in a much larger sum

• Focus on short-term metrics such as break-even and profitability: As discussed above, the primary goal for a startup should be to create defensible value through providing a scalable product, service, or technology. Focusing on these two metrics will often stunt long-term value creation which may limit the investor's return

• Asking for dividends: Startups do not pay dividends as all positive cashflow a company may produce should be put back into the business for further growth

• Failing to add value beyond the money: The best angels provide mentorship, aid in business development, and help with fundraising to further increase the value of the startup

• Focus on physical assets: In general, asset-light startups will be valued higher due to their ability to use capital and scale more efficiently. For many, this may seem counter-intuitive, but the goal of founders is to maximize the return on every dollar raised

That is easier to do through technology than physical assets

• Not aiming high enough: Investors need to recognize that a startup should at least aim to dominate a market. Lowered expectations may stunt the company's growth and make it less attractive to future venture investors

• Funding properly and following up on financial commitments: Investors must allocate capital in no more than two tranches—and not monthly. An investor should want founders to worry about who to hire next or what product feature to add rather than focusing on whether they will be able to pay their employees

To reiterate, the reason an angel invests in a founder is because they trust them. Investors should be there for guidance and support, not to treat them as employees without their own will and direction. Additionally, investors need to remember that if the founders' mental health does not allow them to operate at optimal efficiency, the investor's return will be limited. When we think of the best founders globally, we see the strength of their leadership and the support of their investors through their journey as a key complement to their success.

MANAGING PORTFOLIO RISK

The most important thing to understand is that, while an angel may lose money in the majority of their investments, the ones that are successful should yield a disproportionately positive overall return. So, how does one approach angel investing knowing this? By creating a diversified portfolio. Once a potential investor decides how much money they will allocate to angel investing, the next step is to diversify risk.

For instance, this is how we explain the risk management process to potential angels: if an angel investor has $100,000 to invest, make 5 investments ranging from $15,000 to $25,000. The goal is to champion your portfolio companies' ambitions without the constant risk of failure. Per our previous point, if we allocated $20,000 into five investments, consider the difference between the two following scenarios:

In Scenario A, each of the five investments returns 25% resulting in a total return of $25,000. In Scenario B, however, four of the five investments go to zero—but the fifth investment returns 2,000%, or 20x, bringing in a return of $400,000! This kind of portfolio allocation is what makes angel investors successful.

We remind angel investors that supporting ambitious founders can often result in better returns for an overall portfolio than seemingly safe business models.

The impact of quality angels

When angel investing is done right, its value to the ecosystem and economy as a whole cannot be understated. Think about what percentage of global GDP is attributed to venture-funded startups like Facebook and Google, or the fact that Gojek contributed $7.1 billion to Indonesian GDP in 2019. As angels are a critical component of early stage funding, without their presence, startup ecosystems can be held back. In Bangladesh, the need for greater angel funding is currently a limiting factor for the success of our brilliant, young founders. By increasing local angel capital and bringing in global angels, including NRBs (non-resident Bangladeshis) through networks such as Bangladesh Angels, we can set up our startups for future success.

Quality angel investors can help founders take their companies to the seed stage where they can get further funding from institutional funds, including a vast amount of global capital that is actively looking to enter Bangladesh.

The impact of venture capital is significant to an economy. Companies such as Uber and Facebook had angel investors before they became companies that changed the way we live. In Bangladesh, only a few startups have scaled to a level of national visibility, yet none with the possible exception of bKash are at the level of funding and valuation that regional peers in India or Indonesia have achieved.

For Bangladesh to go from $500 GDP per capita to $1,000, and then $1,000 to $2,000e was achievable with low-level labor arbitrage, but for the country to double from $2,000 to $4,000 and beyond, we'll need to not only nurture home-grown startups but also build a culture of local wealth creation by empowering local founders to move up the value chain and bring in global capital.

In celebration of our country's 50th anniversary, let this next decade be filled with opportunities for every one of us. Let's give our founders the tools to put Bangladesh on the global map as a destination for the startups that may come to shape our collective futures.

The author is the CEO and Founding Partner of Anchorless Bangladesh, an early stage venture investment fund.

Comments