Inflation is not going away anytime soon

The world has entered another era of high inflation, and no country can escape from the heat wave of rising prices. The ghost of the 1970s – termed the Great Inflation – seems to be looming on the horizon. The US, with more than eight percent inflation (never seen in 40 years), is on the lead for inflation, as was the case in the 1970s when the inflation spiral was mainly driven by fuel shock. This time, Russia's invasion of Ukraine kicked off the fuel shock too, but the post-pandemic inflation, which most countries are going through, is not fully related to energy shortage. There are other factors which stoked inflation in the first place before President Putin attacked Ukraine. And those factors will keep inflation high for at least two more years.

First, inflation is a common phenomenon after a big recession. The economy enters the phase of recovery. Output goes up. Higher growth leads to lower unemployment – which in turn gives workers higher power of bargaining. Wages go up and cause wage-push inflation. This is demand-driven inflation, which economists describe as the Phillips curve effect. This is not too bad, because people have jobs, pay is higher, and consumers can afford this inflation. The current inflation is partly attributable to the rising phase of the business cycle. This would have happened to all countries anyway after the Covid-led recession, no matter whether other factors had surfaced or not.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Second, the Covid-led recession is unique in that it triggered supply chain disruptions, which we never saw in the wake of any other recessions. Covid is worse than war. It paused global mobility quite forcibly, but demand remained suppressed. When stricter lockdowns were lifted, the pent-up demand simply exploded. It rushed to hit the market with horrendous desperation, but did not get the products in place. Aggregate demand exceeded aggregate supply, catapulting prices to newer highs every week. This was a golden chance for ballooning up sellers' profits by exploiting the excess demand, and they hit the bull's eye. Since ships transport more than 80 percent of the world's trade volume, and ships take much longer time than flights or trains, the pent-up demand moved fast like a rabbit leaving the turtle-paced supply far behind. And this will continue for more than a year. The typical theory of supply chain management failed because of the very different nature of the recession induced by Covid, never seen before.

Third, the US government infused huge cash in the economy during the recession in the name of multiple stimulus payments. Many others followed suit. This excessive money supply through desperate fiscal deficit has fuelled inflation, as the quantity theory of money asserts. Milton Friedman, who uttered that inflation is always and everywhere a monetary phenomenon, has been correct again. However, Keynes failed to predict American behaviour of saving. Usually, people are supposed to save more when national income goes up, as the theory says. But Americans save less in happy days and more when they feel insecure in hard time. So, a big part of the stimulus money was saved to spend later, and that has hit the market now, exerting an upward pressure on prices. The Federal Reserve won't be able to mop up that excess liquidity soon, enabling inflation to remain high.

Fourth, the Russia-Ukraine war has disrupted not only fuel and gas, but also hurt grain production and exports, sending global commodity and oil prices to higher levels. Only this reason is the same as what caused hyperinflation in the 1970s. This is more so for European countries – most of which are substantially dependant on Russian oil and commodities. While some European countries are 90 percent dependent on Russian oil and gas, the US dependence is as low as 10 percent. Hence, Putin's aggression on Ukraine wouldn't have had much impact on US inflation. Taking a lesson from the 1970s when Middle Eastern countries stopped supplying oil to the US, the American regimes kept on building strategic reserves of oil, which can be as high as 25 percent of their total demand.

Moreover, lessons from the 9/11 attack induced President Barack Obama to forge a new policy for finding self-sufficiency in energy and forcing car manufacturers to ensure fuel efficiency. These reforms have greatly changed the US landscape, so it is not poorly susceptible to external petroleum threats. That is why the Biden administration was capable of being tough on the Kremlin empire to the degree which cannot be imagined by Germany, which remains like a hostage to Russia's energy supply. Russia covers 55 percent of Germany's gas imports and 34 percent of crude oil imports.

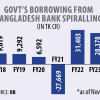

Fifth, as the World Economic Outlook (April 2022) claims, inflation is projected at 5.7 percent in advanced economies and 8.7 percent in emerging market and developing economies in 2022. At the end of 2023, inflation is expected to weaken, but it will still be moderately high in developing nations because of the gradual weakening of their local currencies against the US dollar. This is the channel of imported inflation. And that is more so for Bangladesh, whose effort to keep the value of taka artificially high has nosedived and will fail repeatedly at times ahead, making import prices higher in a gradual fashion. The US Federal Reserve's steps to raise policy rates will further strengthen the US dollar.

Finally, inflation is also driven up by fear or panic – a notion dubbed as expectations-augmented inflation. The media with the right information on prices at different markets and the credible steps by the government can dampen this segment to a great extent. All these factors are present in Bangladesh to trigger inflation and also to keep it stubbornly high until the end of 2023. In addition, Bangladesh's special institutional factors – syndication, hoarding, illicit stocks, and corruption – will exacerbate the situation if the government does not rise against the evils of the market.

Prices, once raised, don't tend to fall that smoothly – a notion that economist John Maynard Keynes termed "downward rigidity" or "stickiness of prices." And that is the case for Bangladesh, suggesting the country's inflation will sustain longer even after the compelling factors weaken or disappear.

Dr Birupaksha Paul is a professor of economics at the State University of New York in Cortland, US, and former chief economist of Bangladesh Bank.

Comments