Budget shows fault lines, not a path out of the crisis

Finance ministers don't possess crystal balls to captivate the audience with mystical allure. They don't have magical foresight. They are real-world agents of economic policy. In times of crisis, which often repeats itself in modern capitalism, they chart a path out of the dark abyss. Sometimes they prove to be successful, sometimes not.

How does Abul Hassan Mahmood Ali measure up to these norms as the new finance minister of Bangladesh? He did try to leave an imprint on our minds, at least by showing the fault lines in the economy and eventually admitting weaknesses, but he blamed almost everything on the global crisis. It was akin to a PR exercise designed to mask the government's own wrongdoing. Economists suggest the new budget is a bland continuation of the past and has failed to carve a way out of the crisis.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

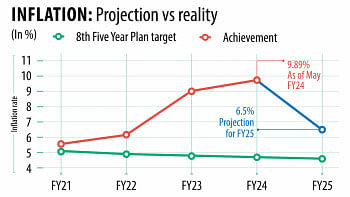

Mahmood Ali acknowledged that the government unsuccessfully tried to tame inflation. Efforts to bridle budget spending alongside a contractionary monetary policy were futile. He attributed stubborn inflation primarily to import-induced price increases and disruptions to the domestic supply chain. But his goal to bring inflation down to 6.5 percent in the fiscal year starting in July from more than 9 percent raised eyebrows.

Bangladesh looks to fiscal consolidation by reducing the budget gap to 4.6 percent of GDP, the narrowest in a decade. The administration vowed to continue belt-tightening, a term hardly used in government circles, in a country perpetually obsessed with growth. This is not to say the government will follow an austere path for too long, as it fears this approach may slow the growth rate.

"Therefore, our goal will be to increase government spending gradually in the second half of the upcoming fiscal year. This will be possible if the revenue realisation increases. To this end, we will lay emphasis on removing tax exemptions gradually," the finance minister said.

The GDP growth target, 6.75 percent, appears to be a decent goal as rating agencies and multilateral lenders have kept the forecast closer to this number. The medium-term growth outlook is favourable, supported by garment exports and stable remittance inflows. In the near term, however, growth may be affected by a lingering dollar shortage.

Amid persistent worry over the economy, the government raised the national budget by 4.6 percent year-on-year to Tk 7,97,000 crore, the slowest pace since Sheikh Hasina's party returned to power in 2009.

Can the budget win back the confidence of local and foreign investors? Very unlikely. That is evidenced by a 14 percent drop in foreign direct investments in 2023 from a year earlier. The trust deficit has also been exposed by the massive sell-off by foreign and local investors. The market lost 1,000 points in just three months, just before the budget, once it allowed investors to sell their shares at will.

Mahmood Ali underlined the need for raising the tax-to-GDP ratio to 10 percent from 8 percent now and upskilling workers going abroad for jobs at the beginning of his speech. But he was conspicuously silent on the runaway banking sector that counted Tk 182,000 crore in non-performing loans, the highest ever.

His path is laden with moral hazard. The government has once again allowed both individuals and companies to whiten black money by paying a 15 percent tax without facing scrutiny. It undermines the government's fight against deep-rooted corruption at a time when excesses by former government officials are in full view.

"The measures such as 'anti-corruption committees' in every metropolis, district, and upazila and 'public hearing' sessions on corruption in government and semi-government offices seem trivial, if not laughable," said Zahid Hussain, former lead economist of the World Bank's Dhaka office.

One of the key concerns is that the government plans to borrow about Tk 137,000 crore from domestic banks to finance its development spending. This is likely to increase the risk of a crowding-out effect as deposits in the banking sector are likely to grow only by Tk 160,000 crore over the next fiscal year.

"In other words, such borrowing targets will raise fiscal dominance in the overall macroeconomic management and will create pressure for the government to resort to central bank financing if such goals are aggressively pursued," said Ashikur Rahman, principal economist at the Policy Research Institute. "It is advisable to rationalise its borrowing target from the banking sector."

TAX PAIN DEEPENS

While the cost of living is high, lower-income families see no light at the end of the tunnel. The minimum tax-free limit remains unchanged in the most difficult times. The burden complicated by increased VAT rates feels heavier when people desperately seek a cushion from unrelenting inflation.

The minister increased the maximum tax rate to 30 percent from 25 percent now for individual payers, "distributing the burden equitably so that higher income individuals pay a larger share of their income or wealth as income tax than lower-income individuals." The corporate tax rate was lowered by 2.5 percentage points, but analysts questioned the benefits given to companies.

The government introduced a prospective tax system in Bangladesh to help expand trade and boost local and foreign investment. The demand for the new system was long-standing, though. It will create some tax predictability. For that, the proposed tax rate for fiscal 2024-25 will be retained for the 2025-26 assessment year. Currently, the country follows a retrospective tax regime.

"I believe that through a prospective tax system, taxpayers can do proper tax planning and help increase tax compliance," the minister said.

The government finally seems to be waking up to the burden of foreign debt. Bangladesh is facing pressure from two sides simultaneously: capital outflows outstrip inflows of funds. That increases the deficit in financial accounts on the one hand and creates the burden of repayment of foreign loans on the other. The interest payment for foreign loans exceeded $1 billion for the first time. The government now fears if the forecast that the interest rate will decline in the United States and other developed nations goes wrong, the trend of higher payment will continue in the future as well. Bangladesh now estimates that the interest payment for foreign loans will swell to $1.86 billion in FY25.

The new budget provides clarity on what's going on in the economy. But the minister shied away from explaining if the crisis reached gale-force intensity and the worst would be over soon.

Are we survivors of the crisis struggling to pick up the pieces? A period of uncertainty creates panic. We expected more than the sense of how we got into this mess. We wanted a roadmap of how to get out of this.

His silence is deafening.

Comments