Why investors not upbeat about bank stocks anymore

Bank stock prices have been low for several years now despite providing handsome annual dividends and this begs the question, why are investors less enthusiastic about buying shares in what was once dubbed the most attractive sector?

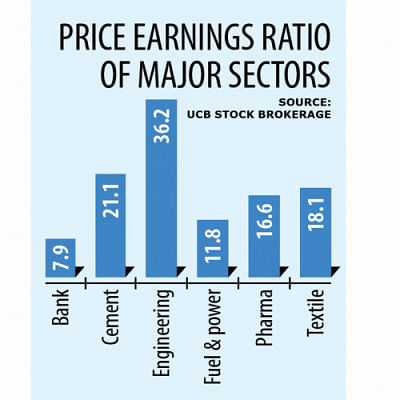

Bank stocks have the lowest overall price-to-earnings (PE) ratio among all 16 sectors in the market as it closed at 7.9 by the end of last week, according to data from Dhaka Stock Exchange (DSE).

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. When the PE ratio of a company or sector is low, it means shares in that company or sector have less value with respect to their profit.

Market players say that banks usually provide 10 per cent to 15 per cent dividend each year and to avail this benefit, investors normally buy shares in the sector from December to February.

Still though, most bank stocks remained flat or moved slowly even in the December-February period for at least the past two years.

Analysts say the three chief reasons why investors lack interest in the sector are the low asset quality of many banks, huge pile up of non-performing loans (NPLs), and Bangladesh Bank's relaxed policies.

Interestingly, another reason for the low demand is that bank stocks are considered non-gambling shares.

Besides, investors are concerned about the sector's future as they believe the profits posted by banks in the country are fictitious, said a stockbroker on condition of anonymity.

"Their 'paper profits' may turn into losses anytime if their asset quality is properly audited," he added.

For example, the People's Leasing and Financial Services, a listed non-bank financial institution, was once a highly profitable company but it has since become a losing concern after failing to repay depositors due to its low asset quality.

Apart from this, banks suffer from huge amounts of default loans while the provision shortfall is also on a rising trend.

"So, the banking sector is not in a good shape," said the stockbroker.

Bangladesh Bank has been taking various measures, such as relaxing the loan rescheduling and classification policies, to reduce the NPL rate but it still surged 16.38 per cent year-on-year to hit Tk 103,274 crore in 2021, as per central bank data.

The ratio of NPLs to outstanding loans and advances stood at 7.9 per cent last year in contrast to 7.6 per cent in 2020, the data showed.

Similarly, the provision shortfall widened to Tk 6,204 crore in September 2021, up 50 times compared to Tk 123 crore in December the year before.

"The full brunt of Covid-19's impact on the banking sector is also yet to be realised thanks to the central bank's policy support," the stockbroker added.

Borrowers enjoyed policy support in 2020 and 2021 as the government stepped in to help them withstand the coronavirus fallout.

For instance, Bangladesh Bank declared a moratorium facility for borrowers throughout 2020 that helped reduce NPLs to Tk 88,734 crore, down 6 per cent year-on-year.

The relaxed policy continued last year as well.

Under the policy, borrowers were allowed to avoid slipping into the default zone in exchange of giving just 15 per cent of the total instalments payable last year.

A top official of a listed bank, preferring anonymity, said it was true that the asset quality of all banks are deteriorating year after year.

Bank loans may turn into sour loans at times for economic reasons but the sad thing is that most of the NPLs were forcefully given even though it was known that the borrowers could default.

"So, the political pressure on banks and influence of their directors should be reduced in order to improve the sector's overall quality," he added.

The banker went on to say that since listed banks float a huge number of shares, these companies are not convenient to gamble with and as a result, investors who wish to engage in such activities end up shunning the sector.

However, some of the listed banks do have good asset quality and show true NPL rates while keeping an adequate provision.

"So, it is not expected for every bank to have low share prices," he said.

Shahidul Islam, chief executive officer of VIPB Asset Management, said there are some irrationalities in the market as good companies sometimes have low share prices while those which perform poorly trade at higher rates.

"Investors should invest seeing the potential of the listed companies," he added.

Among 33 listed banks, 16 which had face values of Tk 10 traded below Tk 15 per share on Wednesday, DSE data showed.

Comments