Bad loans rise in private banks, but drop in state banks

Non-performing loans (NPLs) have increased in private commercial banks but dropped in state-run banks for a portion being regularised through rescheduling.

During the last July-September period, the default loans in private banks rose by Tk 7,902 crore but decreased by Tk 8,657 crore in state-run banks, as per the central bank's latest data.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Overall, the NPLs in Bangladesh's banking sector have slightly decreased, mainly due to the regularisation of some of Janata Bank's loans through rescheduling.

At the end of September, the sector's NPLs stood at Tk 155,397 crore, down by only Tk 642 crore from that in June.

However, when compared year-on-year, the bad loans have gone up by Tk 21,001 crore.

The NPLs of September account for 9.93 percent of the total loan disbursement of Tk 1,565,195 crore.

In reality, default loans have not gone down, rather it increased for some banks in the quarter, said a senior central bank official.

Overall, the default loans have fallen slightly because state-run Janata Bank rescheduled defaulted loans of Beximco and S Alam, two of the country's biggest business groups, during the July-September period, he said.

As a result, default loans in Janata Bank dropped by Tk 11,500 crore, which had a positive impact on the overall sector, said Janata Bank officials.

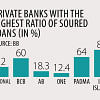

At the end of September, bad loans of state-run banks stood at Tk 65,797 crore whereas it was Tk 81,537 crore in private banks.

In case of foreign banks, it was up from Tk 3,196 crore at the end of June to Tk 3,286 crore at the end of September whereas in specialised banks it ranged from Tk 4,753 crore to Tk 4,777 crore.

A lack of good governance, relaxation of policies pursued by the central bank, political interference and irregularities have largely been responsible for the upward trend of NPLs, as per industry insiders.

Bad loans had hit an all-time high of Tk 156,039 crore at the end of June and continued to rise amidst the withdrawal of central bank relaxation policies on loan classification which were introduced during the pandemic.

On the other hand, bankers say borrowers were simply not interested in repaying bank loans and were using the ongoing economic slowdowns as an excuse.

There is pressure on the economy and the ongoing political turmoil adversely impacted businesses and repayment capacities, Selim RF Hussain, chairman of the Association of Bankers Bangladesh (ABB), told The Daily Star yesterday.

The current forex crisis also slowed down repayments, said Hussain, also managing director of BRAC Bank.

Moinul Islam, a former professor of economics at the University of Chattogram, thinks this was not the actual figure of bad loans because it does not include a huge volume of credit stuck in money loan courts.

"If the entire amount of the loans involved in the court cases and the written-off loans are taken into consideration, the total bad loans in the banking sector will be Tk 450,000 crore," he said recently.

He said the bad loans would not come down unless strict punitive measures were taken against the top defaulters.

Distressed assets in the banking industry amounted to Tk 377,922 crore in 2022, according to the BB's Financial Stability Report 2022.

The distressed assets are calculated considering the total NPLs, outstanding rescheduled and written-off loans.

According to Asian Development Bank, a buildup of the NPLs poses a risk to the health of banks' balance sheets and financial soundness.

The NPLs reduce interest income, lower profitability and deplete banks' capital bases.

They also require higher risk weights and minimum loss coverage in banks' capital requirements, putting a strain on liquidity and increasing funding costs.

With less money available to extend new loans, banks' capacity to lend and make profits is further constrained, it said.

Recently, International Monetary Fund said elevated levels of the NPLs could dampen the growth prospects of Bangladesh.

"A holistic and time bound NPL resolution strategy would help address bank balance sheet weaknesses," it said.

Comments