Can the new leadership save the economy?

It is welcome news that Dr Ahsan H Mansur is going to lead Bangladesh Bank (BB). Former BB governor and current finance advisor to the interim government, Dr Salehuddin Ahmed, will serve as a knowledgeable advisor on finance and banking. The recent addition of a prominent economist like Dr Wahiduddin Mahmud as another new advisor has created a golden opportunity to correct the course of the economy, which is currently in disarray. It would be equally encouraging if the government appoints another expert to lead the Bangladesh Securities and Exchange Commission (BSEC), to represent the country's capital market.

Finally, Dr Muhammad Yunus, head of the interim government and a globally recognised pro-poor growth economist, has the potential to create a powerful leadership team that can not only rescue the economy from a possible downturn, but also guide us toward recovery. Their first task is to address the three groups of looters: bank defaulters, tax dodgers, and money launderers—who have formed a "devil's triangle" and have been coddled by politicians in power, nearly ruining the country's institutions.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

Never has this country seen such a scholarly leadership team for economic policymaking in its history. At times, BB governors were duly qualified, but often the finance ministers or leaders in the capital market were not. On other occasions, both governors and finance ministers were inadequately qualified, placing the wrong people in key positions. This situation weakened the leadership triangle and undermined the effectiveness of the economy.

We know that the leadership team during this interim period is likely to be short-lived, as pressure for new elections is mounting. However, people expect to see a series of reforms in recruitment policies to ensure that only qualified individuals can become BB governor, BSEC chair, or finance ministers—not merely those who curry favour with big-ticket bank looters or who are sycophantic to the regime. People hope that future elected governments will choose scholarly leaders, especially for key financial institutions, whom the public can respect and rely on.

Controlling inflation in the short term and addressing massive youth unemployment in the medium term are their two main challenges. The previous two governors, who questionably held the leading position at the central bank, have made the task for the new governor significantly more difficult. The primary hurdle is to bring clarity and accuracy to the definition of defaulted loans, which were reported as much lower than their actual amount due to looter-friendly definitions. For example, a loan was considered "regular" if only 5 to 10 percent of it was repaid. This is a mockery, and the previous regime approved it easily, primarily so that these defaulters can participate in the one-sided election.

The parliament has largely become a club of corrupt businesspeople who occupy 61 percent of the seats, with the remainder filled by retired bureaucrats, elderly party stalwarts who still crave power, and a few promising youths. Politics has corrupted central-bank policymaking. The finance minister from 2019 to 2023 orchestrated this definitional perversion to favour delinquents, and the past two governors merely complied with the finance minister's wishes without assessing any merit or ethics. The new governor will face resistance from the beneficiary groups when attempting to implement best global practices in loan administration. However, since the finance advisor is not affiliated with any business mafia, the governor will receive wholehearted support from Salehuddin Ahmed whenever corrective measures are undertaken.

Full transparency of information and data should be maintained within the pentagon of leaders to break the "devil's triangle." Governor Mansur is right to emphasise that he will take necessary steps to ensure that financial hooligans who siphoned off millions of dollars from the country face serious consequences. Since the interim government is not concerned with political popularity, it is crucial for it to reveal true figures on inflation, unemployment, defaulted loans, written-off loans, money trafficking, and revenue gaps. This transparency will aid other agencies and researchers in working effectively. Hiding data has caused serious damage to the economy, though ministers adopted this tactic to remain politically expedient.

This is the time to abolish the Financial Institutions Division at the ministry. Its establishment after 2009 has caused more harm than good by weakening the central bank and empowering finance ministry officials who often served politically connected top-ranking oligarchs, including those who closely supported the former prime minister. Moral hazards have reached such a point that making a U-turn will be one of the toughest tasks for the interim government. It is also crucial to establish "Revenue" as an independent ministry, as it represents more than 10 percent of GDP. This is a significant weak point in Bangladesh's finance sector that has been long ignored. Leading such a crucial department with just non-expert bureaucrats has proven ineffective and will continue to do so.

In other countries, defaulted loans rise when the economy performs poorly. Bangladesh's growth continued to rise until 2019, reaching nearly 8 percent. Growth has become lacklustre after Covid-19, not due to global factors but because of increased wilful defaults and rampant corruption across all sectors. Still, growth has hovered around 5 to 6 percent, which does not justify requests for loan rescheduling or default. The nature of defaulted loans varies widely based on ownership structure, indicating that they are primarily institutional and political in nature, rather than being related to the real economy.

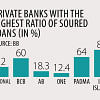

The share of defaulted loans out of total outstanding loans is as low as 3.38 percent in foreign banks, while it is as high as 22 percent in private banks. The corresponding figure for public banks is abnormally high at 38.56 percent, vindicating that the issue is primarily one of poor governance and political looting. The new governor is expected to address this problem. All boards of directors at both public and private banks must be reshuffled, and the directorship law should be revoked.

Professor Rehman Sobhan mentioned in a seminar on the banking sector on July 7 this year that Bangladesh Bank (BB) enjoyed a rich tradition of having scholars as governors, such as Dr Mohammed Farashuddin, Dr Fakruddin Ahmed, Dr Salehuddin Ahmed, and finally Dr Atiur Rahman. This tradition collapsed in 2016, leading to less favourable results in the banking industry. However, with the appointment of Ahsan H Mansur as governor, we hope that BB will regain its knowledge-based leadership and that subsequent regimes will uphold this standard, which is crucial for the economy to thrive.

Dr Birupaksha Paul is professor of economics at the State University of New York in Cortland, US.

Views expressed in this article are the author's own.

Follow The Daily Star Opinion on Facebook for the latest opinions, commentaries and analyses by experts and professionals. To contribute your article or letter to The Daily Star Opinion, see our guidelines for submission.

Comments